You already know the truth about annuity sales leads. Most of them are garbage. You've probably burned through thousands of dollars buying leads that turned out to be tire-kickers, people who filled out a form while half-asleep, or prospects shopping for free information with no intention of buying. The entire annuity lead industry has a credibility problem, and you're stuck in the middle trying to hit your production goals while figuring out which lead sources actually deliver people ready to have a real conversation about retirement income.

Here's what nobody tells you upfront: the problem isn't just lead quality. It's that most advisors treat lead generation and lead nurturing as separate activities, when they're actually two halves of the same system. You can't just buy a list, make some calls, and expect conversions. And you can't just create content and hope the right people find you. The advisors who consistently write annuity business have systems that do both - and they've stopped thinking about "leads" as a commodity they purchase and started thinking about prospect pipelines they build.

Why Most Annuity Sales Leads Don't Convert

Let's start with the uncomfortable reality. When you buy annuity sales leads, you're usually getting one of three things: aged leads that have been resold multiple times, survey responses from people who don't remember filling anything out, or legitimate inquiries that are being sent to 8-12 other agents simultaneously.

The math doesn't work in your favor. If you're paying $25-75 per lead and closing at 2-5%, you need extremely high premium cases just to break even on your lead cost. And that's before factoring in your time.

The bigger issue is context. Most purchased leads lack the situational awareness that makes a conversation productive. You don't know:

- What triggered their inquiry

- What they've already researched

- What their actual timeline is

- Who else they're talking to

- What misconceptions they're carrying

You end up spending the first 20 minutes of every call doing discovery that should have happened before you ever picked up the phone.

The Lead Quality Problem Nobody Talks About

Here's the pattern you've probably experienced: You call a lead within 5 minutes of receiving it. The prospect answers. They confirm they're interested in learning about annuities. Then they say, "Can you just email me some information?"

That's not a bad lead. That's an uneducated prospect who doesn't know what questions to ask yet. The traditional sales approach treats this as a dead end. The systems approach treats this as the beginning of a nurture sequence.

The advisors who win in 2026 understand that most annuity sales leads aren't ready to buy when they first raise their hand. They're ready to learn. And if you can be the one who educates them without being pushy, you'll be the one they call when they're ready to move forward.

Building Your Own Annuity Lead Generation System

Stop thinking about leads as something you buy. Start thinking about them as something you cultivate. The best lead generation strategies for annuity agents focus on attraction rather than interruption.

Here's what a modern annuity lead generation system looks like:

Educational Content as the Entry Point

You need assets that answer the questions your prospects are already asking:

- "How do annuities actually work?"

- "What makes a fixed indexed annuity different?"

- "How much of my retirement savings should be in an annuity?"

- "What happens if I need my money back?"

These aren't sales presentations. They're pre-sales education. When someone watches a 3-minute video explaining how annuity fees work, they're self-qualifying. They're telling you they're willing to invest time in understanding the product.

Structured Follow-Up Sequences

Once someone enters your system, they need consistent touchpoints. Not daily sales calls. Structured education delivered over 2-3 weeks that builds context and trust.

A typical sequence might look like:

- Day 1: Confirmation email with foundational concept video

- Day 3: Common misconceptions article

- Day 7: Case study or client story

- Day 10: Product comparison guide

- Day 14: Invitation to schedule a strategy session

Each piece of content should stand alone and provide value, but together they create a knowledge foundation that makes your eventual sales conversation 10x more productive. This is similar to what successful advisors do when they build consistent marketing systems that generate predictable pipeline.

The Discovery-First Approach

Traditional lead generation asks for contact information. Modern lead generation asks discovery questions first. Before someone ever gets on a call with you, they should be answering questions about:

- Current retirement assets and where they're held

- Income needs and timeline

- Risk tolerance and previous investment experience

- Tax situation and legacy goals

- Concerns about market volatility or longevity

When you collect this information through a structured questionnaire before the first call, two things happen: prospects who aren't serious drop out, and prospects who are serious show up to your call already thinking about their specific situation rather than asking generic questions.

Where to Find Quality Annuity Sales Leads

If you're going to buy leads, you need to know what separates quality sources from lead mills. Here's the breakdown.

| Lead Source | Average Cost | Exclusivity | Conversion Expectation | Best For |

|---|

| Exclusive purchased leads | $75-150 | You only | 5-12% | High-touch advisors with strong follow-up |

| Shared leads | $15-40 | 3-10 agents | 2-4% | Volume players with quick response systems |

| SEO/organic inquiries | Time investment | You only | 15-30% | Advisors willing to invest in long-term content |

| Client referrals | Free-$500 (referral reward) | You only | 40-60% | Established advisors with happy clients |

| Seminar attendees | $50-200 per attendee | You only | 10-20% | Advisors comfortable with group presentations |

The problem with most lead purchasing isn't the channel itself. It's that advisors buy leads without having a nurture system in place. You can't just call, pitch, and close anymore. The internet has made prospects too sophisticated.

What to Look For in Purchased Leads

If you're buying annuity sales leads, insist on:

- Real-time delivery - Leads older than 15 minutes lose 80% of their value

- Source transparency - Know exactly where the lead came from

- Data completeness - Age, assets, current holdings, and specific interest area

- Exclusivity guarantees - Or at least know how many agents you're competing against

- Return/refund policy - Good lead vendors stand behind their product

Before you spend serious money, test small. Buy 10-20 leads from a new source and track them through your full sales cycle. What percentage answer? What percentage agree to a meeting? What percentage actually show up? What percentage result in submitted applications?

Those metrics tell you whether a lead source is worth scaling.

Organic Lead Generation That Actually Works

The advisors who've stopped buying leads entirely didn't do it because they're marketing geniuses. They did it because they built systems that generate inbound interest consistently. For insights on what independent agents are doing, check out these effective annuity sales strategies being used in 2026.

SEO and Educational Content

When someone searches "should I put my 401k rollover into an annuity," they're not ready to buy. But they're 6-12 months away from a decision. If your content answers that question better than anyone else's, you become the trusted source they return to as they move through their research process.

This isn't about blogging for the sake of blogging. It's about creating content that answers the exact questions your ideal prospects are asking Google.

Video as a Qualification Tool

Here's where most advisors miss an opportunity. You send someone a PDF or article, and you have no idea if they read it. You send someone a video, and you can see exactly how much they watched.

When a prospect watches 80% of a 5-minute video explaining annuity surrender periods, that's a signal. They're engaged. They're educating themselves. That's the prospect you want to call.

Better yet, when you use video systematically throughout your nurture process, prospects arrive at sales conversations already familiar with your communication style and expertise. You're not a stranger cold-calling them. You're the advisor they've been learning from for three weeks.

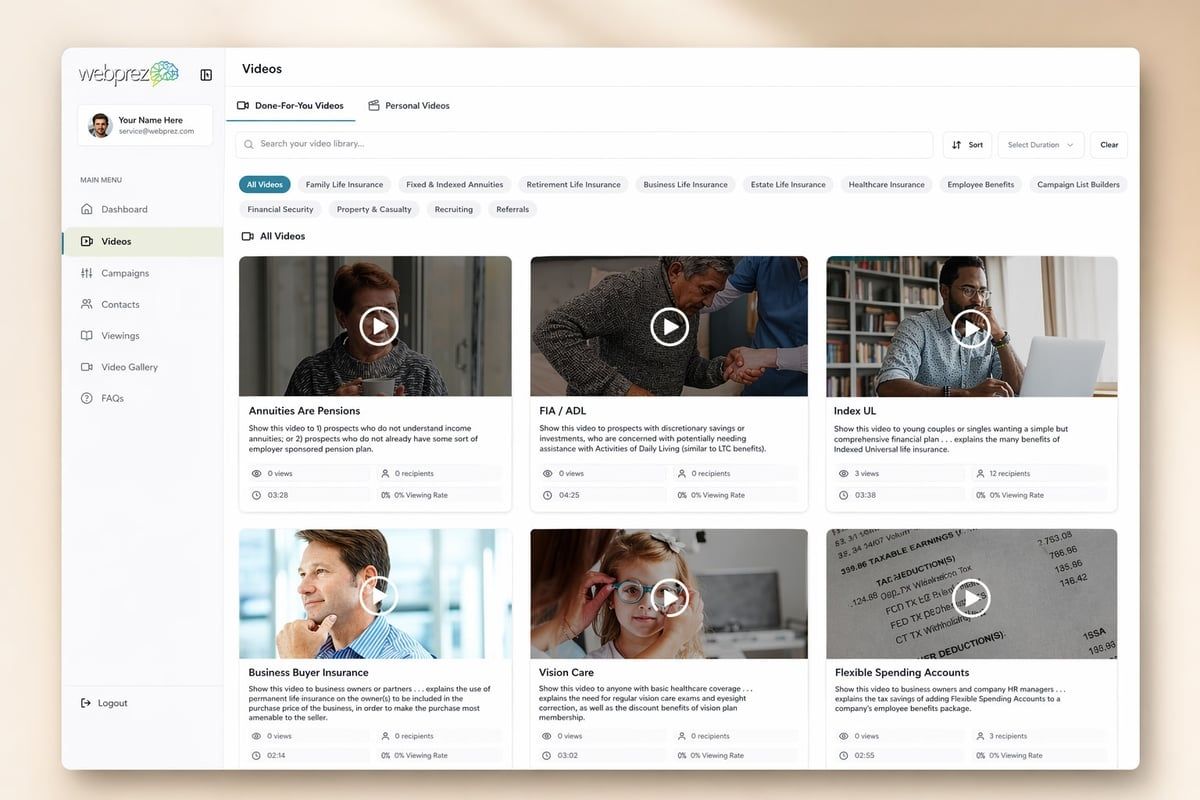

The WebPrez Video Library includes short-form client education videos across annuities, retirement income, and estate planning designed specifically for this kind of pre-meeting education. Advisors use these videos to start conversations and qualify interest before investing time in formal appointments.

How to Qualify Annuity Sales Leads Before You Waste Time

Not every inquiry deserves an hour of your time. The fastest way to improve your conversion rate is to stop spending time on prospects who aren't qualified. Here's how to filter effectively.

Financial Qualification Criteria

At minimum, a qualified annuity prospect should have:

- Liquid assets of $100,000+ - Below this, annuity solutions often don't make mathematical sense

- Age 50+ - Younger prospects rarely benefit from annuities given their time horizon

- Income stability or proximity to retirement - Active income replacement needs

- Clear pain point - Fear of loss, sequence of returns risk, income gap, or tax burden

If a prospect doesn't meet these criteria, they might be a good candidate for other products, but they're probably not a good annuity fit right now.

Behavioral Qualification Signals

Beyond demographics and assets, watch for behavioral signals that indicate serious interest:

- They consume content you send them

- They respond to emails within 24-48 hours

- They ask specific questions rather than general ones

- They mention a timeline or triggering event

- They've spoken to other advisors (shows they're actively evaluating)

One of the strongest qualification methods is a structured discovery questionnaire. When prospects are willing to spend 10-15 minutes answering detailed questions about their financial situation before a call, they're self-selecting for seriousness.

The Discovery Conversation Framework

When you do get on the phone with a qualified annuity lead, your job isn't to pitch. It's to diagnose. Here's a framework that works:

Current Situation Analysis

- Where are your retirement assets currently held?

- What's your current income replacement strategy?

- What keeps you up at night about your retirement plan?

Future State Vision

- What does financial security look like for you in retirement?

- How much guaranteed income would eliminate your worry?

- What legacy goals do you have?

Gap Identification

- What's the difference between where you are and where you want to be?

- What's preventing you from bridging that gap right now?

This isn't a script. It's a thinking framework. Your goal is to understand their situation well enough that when you eventually present a solution, it feels like the obvious answer to the problems they just articulated. Understanding how to sell annuities effectively starts with mastering these discovery conversations.

Converting Leads Into Annuity Sales

You've generated the lead. You've qualified them. You've had a good discovery conversation. Now what? This is where most advisors fumble. They jump straight to product presentation without bridging the gap between discovery and recommendation.

The Snapshot Approach

Before you present any product, give the prospect a clear picture of their current situation. This could be a one-page visual showing:

- Current assets and allocation

- Income sources in retirement

- Gap between expenses and guaranteed income

- Longevity risk exposure

- Sequence of returns vulnerability

When a prospect sees their situation visualized, two things happen: they stop thinking abstractly about retirement and start thinking specifically about their numbers, and they become receptive to solutions that address the gaps you've identified together.

Product Recommendation as Problem Solution

Never lead with product features. Always lead with how the product solves the specific problem you identified in discovery.

Instead of: "This fixed indexed annuity offers 6% guaranteed growth for 10 years..."

Try: "Remember how you mentioned you're worried about another 2008 happening right when you retire? Here's how we can eliminate that risk for the portion of your money earmarked for income..."

The product becomes the answer to their stated concern, not a sales pitch you're delivering.

Handling Common Objections Upfront

The best way to handle objections is to address them before the prospect raises them. In your presentation, proactively discuss:

- Liquidity concerns: "You're probably wondering what happens if you need this money..."

- Fee transparency: "Let me show you exactly how this is compensated..."

- Surrender periods: "Here's why the commitment period exists and how it protects your guarantee..."

When you bring up the objection first, you control the framing. You're not defensive. You're thorough. Learn more about converting annuity leads into actual sales with proven follow-up and retargeting approaches.

Follow-Up That Actually Closes Business

Most annuity sales aren't won in the first meeting. They're won in the follow-up. But most advisors treat follow-up as "checking in" rather than as a structured progression toward a decision.

A proper follow-up sequence includes:

- Same-day recap - Email summarizing what you discussed and next steps

- 48-hour value add - Send a resource relevant to their specific situation

- One-week strategy outline - Written recommendation with options

- Two-week decision framework - Help them evaluate their choice criteria

- Three-week conversation - Schedule call to address remaining questions

Notice that none of these steps are "just following up." Each one delivers something. Each one moves the conversation forward. Each one makes it easy for the prospect to say yes.

What Smart Advisors Are Doing Differently in 2026

The annuity market has changed. The advisors who are thriving have adapted their approach to match how modern prospects research and make decisions. For broader context, see what's working in financial advisor marketing strategies this year.

They've Stopped Chasing and Started Attracting

Top producers aren't cold-calling annuity sales leads anymore. They're creating educational ecosystems that attract pre-qualified prospects who've already consumed hours of their content before the first conversation.

This doesn't mean they don't buy leads. It means when they do buy leads, those leads enter a nurture system rather than a sales pitch.

They Use Technology to Scale Personal Touch

The best advisors are using CRM systems that track:

- Which videos prospects watched

- Which emails they opened

- Which pages on their website they visited

- When they're most likely to engage

This behavioral data tells them when a prospect is getting serious, allowing them to time their outreach perfectly rather than making blind follow-up calls.

They've Standardized Their Education Process

Instead of reinventing the wheel for every prospect, successful advisors have standardized educational sequences. Same videos. Same articles. Same case studies. Same discovery process.

This isn't about being robotic. It's about being efficient. When your education process is standardized, you can focus your creative energy on the parts that matter: understanding each prospect's unique situation and crafting personalized solutions.

| Traditional Approach | Systems Approach |

|---|

| Buy leads → Call immediately → Pitch product | Generate interest → Nurture with education → Diagnose situation |

| Measure success by contact rate | Measure success by conversion rate |

| Treat each prospect as unique from scratch | Use standardized education, customize solutions |

| Focus on features and rates | Focus on problems and outcomes |

| Hope for referrals | Systematically request and receive referrals |

They Treat Existing Clients as Lead Sources

The absolute best annuity sales leads come from people who already bought from you. Client referrals convert at 40-60% compared to 2-5% for cold leads. Yet most advisors have no systematic approach to generating referrals.

The advisors who've cracked this code do three things:

- They ask for referrals at the right moment (after delivering value, not when onboarding)

- They make it specific ("Who else do you know planning retirement in the next 2-3 years?")

- They make it easy (provide a simple intro email the client can forward)

Frequently Asked Questions

What's a realistic conversion rate for annuity sales leads?

It depends entirely on the lead source and your follow-up system. Purchased shared leads typically convert at 2-4%. Exclusive leads convert at 5-12%. Organic leads from your website or content convert at 15-30%. Client referrals convert at 40-60%. If you're below these benchmarks, the problem is usually follow-up process, not lead quality. Most advisors give up after 2-3 contact attempts when research shows it takes 8-12 touchpoints to convert a cold lead into a client.

Should I buy aged annuity leads?

Only if you have a strong nurture system and you're buying them at deep discounts ($5-10 each). Aged leads have been contacted by multiple agents and are often skeptical or no longer in-market. However, if you can re-engage them with educational content rather than sales pitches, some percentage will respond. The math only works if you're paying very little and treating them as long-term nurture candidates rather than hot prospects. Before buying any leads, understand what advisors need to know before purchasing.

How quickly should I contact a new annuity lead?

If it's a real-time exclusive lead, within 5 minutes. Response rates drop 80% after 30 minutes. If it's a shared lead, within 15 minutes. If it's a marketing-generated lead (from your website or content), within 2 hours during business hours. The speed matters less than having a structured first touchpoint. Your immediate goal isn't to pitch - it's to confirm interest, set context, and schedule a proper discovery conversation.

What's the best way to generate annuity leads without buying them?

Educational content marketing consistently outperforms purchased leads in quality and cost-effectiveness. Start by creating content that answers the questions your prospects are already asking: how annuities work, when they make sense, how to evaluate options, what to watch out for. Publish this as blog posts, videos, and downloadable guides. Use SEO to rank for terms like "annuity rollover options" or "fixed indexed annuity explained." Add a simple lead capture offering a retirement income analysis or annuity comparison guide. This approach takes 6-12 months to gain traction but generates leads that cost you time rather than cash and convert at much higher rates. Learn strategies for increasing annuity appointments without buying leads.

How many touches does it take to convert an annuity lead?

Industry data shows it takes an average of 8-12 touchpoints to convert a cold lead into an annuity client. Most advisors give up after 2-3 attempts, which is why their conversion rates are terrible. Your touches should mix value (educational content, market updates, case studies) with calls to action (schedule a call, download a guide, watch a video). Space them out over 4-8 weeks rather than cramming them into one week. The goal is to stay top-of-mind while building trust through consistent, helpful communication rather than aggressive selling.

Annuity sales leads will always be a numbers game, but the advisors who win are the ones who've built systems that improve the numbers. Stop thinking about leads as a one-time purchase and start thinking about prospect development as an ongoing process. When you combine smart lead generation, structured education, and disciplined follow-up, your conversion rates will climb and your cost per client will drop. WebPrez helps advisors systematize this entire process with curated video content, campaign templates, and the Smart Money System framework - turning complex annuity concepts into clear client conversations that move prospects from confused to confident.