Selling annuities isn't rocket science, but it does require a system. You can't wing it when you're asking someone to commit hundreds of thousands of dollars to a product they barely understand. The advisors consistently writing annuity business aren't necessarily the smoothest talkers or the most aggressive closers. They're the ones who've built a repeatable process that moves prospects from confusion to confidence without creating friction.

The problem? Most advisors approach selling annuities like they're selling a mutual fund or a term life policy. They jump straight to features and benefits before uncovering whether the client even has a problem worth solving. Then they wonder why prospects ghost them or say they need to "think about it."

This guide walks through the actual mechanics of selling annuities in 2026, from the first discovery conversation to getting the check. No fluff. No motivational nonsense. Just the framework you can implement this week.

Also read, How To Sell Annuities article...

Understanding What You're Really Selling

Here's the uncomfortable truth: you're not selling annuities. You're selling certainty in an uncertain world.

When a client buys an annuity, they're buying protection from outliving their money, market crashes during retirement, or the stress of managing distributions themselves. The annuity is just the delivery mechanism.

This distinction matters because it changes how you position the conversation. You're not leading with products. You're leading with problems the client doesn't want to experience.

The advisors struggling with selling annuities usually make one of three mistakes:

- They explain the product before identifying the fear

- They oversell guarantees without addressing trade-offs

- They assume the prospect understands why they need one

None of these approaches work anymore. Clients in 2026 have access to more information than ever, which paradoxically makes them more confused, not less.

The Three Client Types You'll Encounter

Not everyone needs an annuity, and not everyone who needs one will buy. Understanding which type you're talking to saves you hours of wasted effort.

The Income-Focused Retiree: They're already retired or within 24 months. Their biggest fear is running out of money before they run out of life. They need predictable income and hate volatility. These prospects are your best fit for immediate or deferred income annuities.

The Market-Skeptical Accumulator: Still working, maybe 5-10 years from retirement. They've been burned by market corrections and want growth without the downside. Fixed indexed annuities resonate here, but you have to address liquidity concerns upfront.

The Legacy Planner: They've got enough to live on. Now they're thinking about heirs, taxes, and leaving something behind efficiently. Annuities with death benefit riders or as part of a pension maximization strategy make sense, but only after you've solved for their income needs first.

Building Your Discovery Framework

Discovery is where selling annuities actually happens. The presentation is just confirmation.

Most advisors ask surface-level questions and wonder why they can't uncover real opportunities. They ask, "How do you feel about your retirement plan?" instead of "What keeps you up at night about money?"

Here's a better framework, broken into three phases:

Phase One: Current State Assessment

Start by mapping what they have, not what they need. This removes defensiveness and gives you a baseline.

- What accounts do they currently have (401k, IRA, brokerage, CDs)?

- How much do they have in each bucket?

- What's their current withdrawal strategy, if any?

- Who manages this money right now?

Don't rush this. Clients need to feel heard before they'll hear you. This phase builds trust and uncovers gaps they didn't know existed.

Phase Two: Fear and Priority Identification

Now you dig into what actually matters to them. These questions feel uncomfortable to ask, but they're essential:

- "If the market dropped 30% next year, how would that impact your retirement timeline?"

- "What's your plan if you live to 95 and your portfolio doesn't?"

- "How much monthly income do you need to feel secure, not just survive?"

Notice the pattern? You're asking them to visualize specific failure scenarios. This isn't fear-mongering. It's helping them see the gap between their current plan and their actual needs.

Phase Three: Solution Criteria Development

Before you mention annuities, get them to define what a good solution would look like:

- "If you could guarantee a certain amount of monthly income, what number would let you sleep better?"

- "How important is liquidity to you versus certainty?"

- "Would you trade some upside potential for downside protection?"

When they answer these questions, they're building their own case for an annuity. You're just connecting the dots.

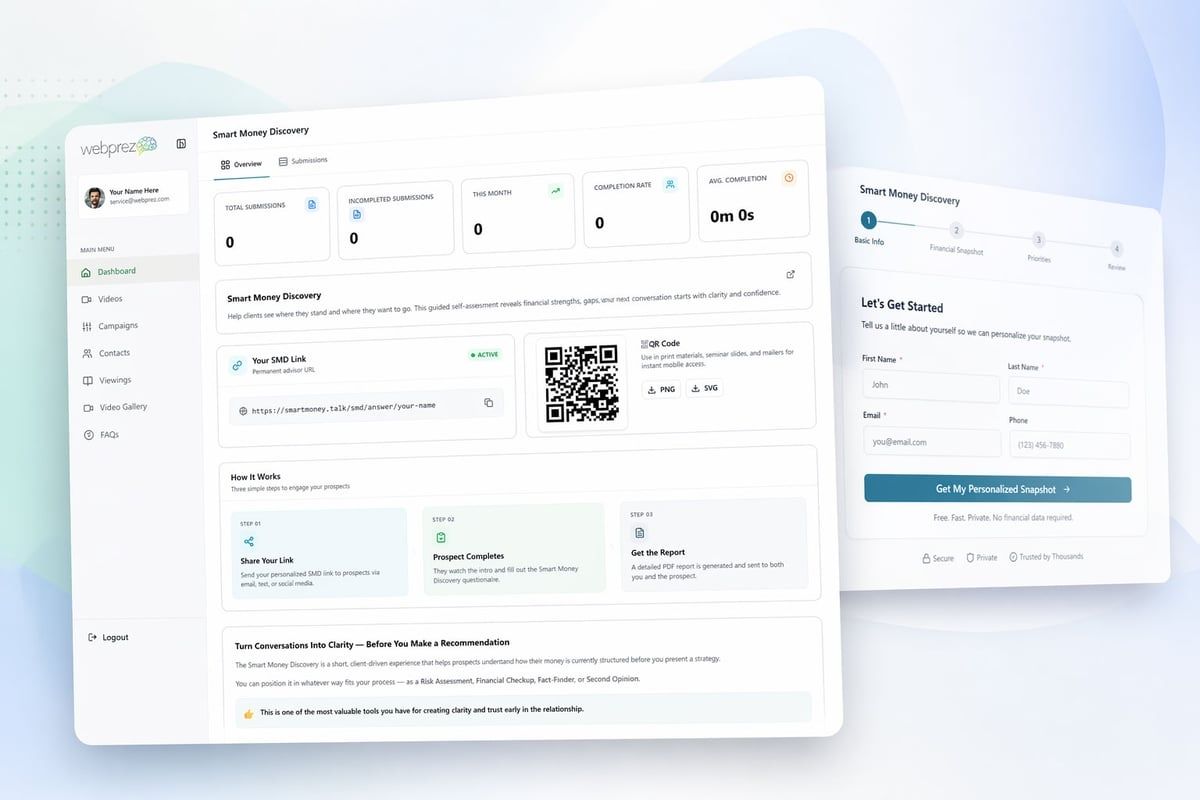

The Smart Money Discovery framework inside WebPrez automates much of this process, generating a personalized financial snapshot that surfaces gaps without making you ask awkward questions manually.

Presenting the Solution Without Losing Them

You've done great discovery. You know their fears, priorities, and current gaps. Now comes the part where most advisors blow it: the presentation.

The biggest mistake? Explaining how annuities work instead of how this specific annuity solves their specific problem.

Here's the structure that works:

Start With the Problem They Told You About

"You mentioned you need $6,000 a month in guaranteed income to cover your essentials, but right now you're only getting $3,200 from Social Security. That leaves a $2,800 gap that you're covering from your portfolio. What happens if the market tanks right when you need that money?"

See what happened there? You didn't say "annuity" once. You just restated their problem in specific numbers.

Present the Annuity as One Solution, Not the Only One

Give them options. This builds trust and reduces sales resistance.

| Solution | Guaranteed Income | Liquidity | Market Exposure |

|---|

| Continue current plan | None | Full | Full |

| Immediate annuity | $2,800/month | Limited | None |

| Deferred income annuity | $3,400/month (starting at 70) | Moderate | None |

When you present choices, prospects feel more in control. They're making a decision, not being sold.

Address Trade-Offs Before They Ask

"The trade-off here is liquidity. You're locking up $400,000 to generate that income. You won't be able to access that principal easily. But in exchange, you get certainty. No market can take that $2,800 away from you."

Advisors who close consistently don't hide the downsides. They own them. They explain why the trade-off makes sense for this specific client's situation.

Handling the Real Objections

"I need to think about it" is not an objection. It's a symptom of one of three things: they don't trust you, they don't understand it, or they don't see the urgency.

Here are the real objections and how to handle them:

"What if I die early? I lose all that money."

Translation: They're worried about making a bad bet on their longevity.

Response: "That's exactly why we structure this with a period certain or death benefit rider. If something happens to you in the first 15 years, your spouse or beneficiaries get the remainder of the payments. You're not betting against yourself. You're protecting against living too long."

"Rates could go up. I should wait."

Translation: Fear of missing out on better terms later.

Response: "You're right, rates might improve. They might also drop. But here's what I know: you need $2,800 a month to cover your bills regardless of what rates do. Waiting doesn't solve that problem. It just extends the period where you're at risk."

According to LIMRA's latest data, annuity sales hit record levels precisely because advisors are getting better at framing the conversation around client needs, not product features.

"I heard annuities are expensive and full of fees."

Translation: They read something online or talked to a fee-only advisor who doesn't sell them.

Response: "Some are, absolutely. That's why we're looking at a single-premium immediate annuity with no ongoing fees. You pay once, you get income for life. No asset management fees, no annual costs. The 'expense' is the spread the insurance company takes in exchange for the guarantee. It's built into the payout rate."

Then show them the math. Transparency beats defensiveness every time.

The Mechanics of Getting to Yes

You've presented the solution. You've handled objections. Now you need to close without being pushy.

The best closers don't ask for the sale. They assume the next step and confirm logistics.

The Assumptive Close

"Based on what you've told me, the immediate annuity with the 15-year period certain makes the most sense. I'll need a few things from you to get the application started: a recent statement from your IRA and about 30 minutes to fill out the paperwork. Does Thursday afternoon or Friday morning work better?"

Notice you didn't ask if they want to move forward. You asked when they want to move forward.

The Trial Close

If you're not sure they're ready, use a trial close to test the temperature:

"If we could lock in that $2,800 a month guaranteed, is there anything else you'd need to see before moving forward?"

Their answer tells you exactly what's left to resolve. Either they say "no, let's do it," or they surface the real remaining objection.

Following Up Without Being Annoying

If they're not ready to commit on the spot, you need a follow-up system that doesn't rely on you remembering to call them.

Set a specific next step before they leave:

"I'm going to send you a one-page summary of what we discussed today and the three options we looked at. Can you review it by Wednesday, and I'll call you Thursday morning to answer any questions?"

Then actually send that summary. A simple email with bullets recapping their problem, the solutions you discussed, and the trade-offs of each option.

Using structured marketing frameworks ensures no prospect falls through the cracks and every follow-up feels personalized, not automated.

Compliance and Documentation That Protects You

Selling annuities comes with regulatory scrutiny. You need documentation that proves suitability and protects you if a client's heirs decide to make trouble.

Suitability Documentation Checklist

Every annuity sale should have these elements documented in your CRM or client file:

- Discovery notes: What they said they needed, in their words

- Product comparison: Why you recommended this annuity over alternatives

- Trade-off acknowledgment: Proof they understood liquidity restrictions, surrender charges, or other limitations

- Beneficiary designations: Documented and signed

- State-specific forms: Varies by state, but many require additional disclosures for seniors

This isn't optional. It's the difference between a smooth transaction and a compliance nightmare three years from now.

Best Practices for Electronic Applications

Most carriers now offer electronic applications that speed up the underwriting process. Here's how to avoid common mistakes:

- Verify account titles match exactly (IRA vs. Roth IRA matters)

- Confirm beneficiary Social Security numbers before submitting

- Use the client's email address, not yours, for carrier communications

- Keep a PDF copy of every submitted application

One wrong digit on a Social Security number can delay processing by weeks. Triple-check before you hit submit.

Building a Repeatable System

The advisors writing consistent annuity business aren't winging it every time. They've built systems that make selling annuities predictable and scalable.

Campaign-Based Prospecting

Instead of hoping someone asks about annuities, create educational campaigns that identify interested prospects:

- Month One: Send a video explaining the difference between SPIAs, DIAs, and FIAs

- Month Two: Share a case study of a client who solved their income gap

- Month Three: Offer a retirement income analysis or gap assessment

The prospects who engage with all three pieces of content are telling you they're interested. Now you have a warm conversation starter.

The WebPrez Video Library includes pre-built annuity education videos across multiple categories, making it easy to deploy these campaigns without creating content from scratch.

Template-Based Presentations

Create three core presentation templates:

- Income Gap Analysis: For prospects who need guaranteed income

- Pension Maximization: For couples deciding between lump sum and pension

- Legacy Optimization: For clients using annuities in estate planning

Each template should have:

- A one-page visual showing their current state vs. future state

- A comparison table of solution options

- Pre-written email follow-up language

This isn't about being robotic. It's about having a proven framework you can customize for each client without starting from scratch every time.

Batch Processing Applications

Don't submit annuity applications one at a time as they come in. Batch them weekly.

Set aside Thursday afternoons for application processing. Knock out all your paperwork in one focused session instead of context-switching throughout the week.

This small operational tweak can double your capacity without working more hours.

Common Mistakes That Kill Annuity Sales

Even experienced advisors fall into these traps. Here's what to avoid:

Mistake #1: Selling Product Features Instead of Solutions

Clients don't care about participation rates, caps, or spreads until they understand why those things matter to their situation.

Lead with the outcome: "You need $X per month guaranteed." Then explain how the product delivers that outcome.

Mistake #2: Overselling Guarantees

Yes, annuities offer guarantees that market-based investments don't. But guarantees have costs.

If you don't explain the trade-offs transparently, you create unrealistic expectations. Then the client gets buyer's remorse when they realize they can't access the money.

Mistake #3: Not Reviewing Existing Annuities

Many of your prospects already own annuities they bought 10-20 years ago. Those contracts often have outdated terms or high fees.

Reviewing old annuities can uncover significant opportunities to improve client outcomes while generating new business through exchanges or rollovers.

Mistake #4: Ignoring the Spouse

If you're selling a joint-life annuity or the couple is married, both spouses need to understand and agree to the decision.

Selling to one spouse while the other sits there confused is a recipe for cancellations and complaints.

Mistake #5: No Post-Sale Follow-Up

The sale isn't over when the check clears. It's over when the client receives their first payment and confirms they made the right decision.

Schedule a 90-day check-in to review how everything is working. This prevents buyer's remorse and generates referrals.

Why Annuities Are Having a Moment

If you've noticed more prospects asking about annuities lately, you're not imagining it. Market conditions and demographic shifts have created a perfect storm for annuity sales.

Rising Interest Rates Make Annuities Attractive Again

For years, annuities offered terrible payout rates because interest rates were at historic lows. That's changed.

Higher rates mean better income payouts, making annuities competitive with other fixed-income options. Prospects who dismissed annuities five years ago are now asking about them.

As MoneyWeek recently reported, annuities are experiencing a resurgence as retirees seek stability in volatile markets.

Baby Boomers Are Entering the Distribution Phase

The largest generation in history is moving from accumulation to distribution. They're not asking "how do I grow this?" anymore. They're asking "how do I not lose this?"

That's an annuity conversation waiting to happen.

Market Volatility Has Destroyed Confidence

The last few years have shown even diversified portfolios can experience dramatic drawdowns. Retirees who watched their account balances drop 20-30% are now prioritizing certainty over growth.

This shift in mindset makes selling annuities easier because you're offering what they're already looking for.

Common Myths You'll Need to Debunk

Despite growing interest, annuities still carry baggage from decades of bad press and poor sales practices. You'll need to address these myths head-on.

Kiplinger's guide to annuity myths is a helpful resource to understand the most common misconceptions your clients bring to the table.

Myth: "Annuities are too expensive."

Reality: It depends on the type. Immediate annuities have minimal costs. Variable annuities can be expensive if loaded with riders. Compare apples to apples.

Myth: "I lose my money if I die early."

Reality: Only if you choose a life-only payout. Period certain and death benefit options protect beneficiaries.

Myth: "Annuities aren't safe."

Reality: They're backed by insurance company reserves and state guarantee associations. Understanding the actual safety mechanisms helps clients make informed decisions.

FAQ: Selling Annuities in Practice

How do I know if a client is a good fit for an annuity?

Look for three signals: they're within 5 years of retirement or already retired, they express anxiety about market volatility, and they have at least some assets they don't need for liquidity. If they check all three boxes, start the conversation. If they don't, explore other solutions first.

What's the best way to explain surrender charges without scaring prospects away?

Frame them as the trade-off for the guarantee. Say something like: "The insurance company can offer this guaranteed income because they know you're committing the money for a specific period. The surrender charge protects them from having to liquidate long-term investments to give you your money back early. It's steep in the first few years and phases out over time. That's why we only use money you don't need for emergencies."

How long should the sales process take from first conversation to application?

For a straightforward case, two to three meetings over 2-4 weeks. First meeting is discovery. Second meeting is presentation and comparison. Third meeting is application. If it's dragging beyond a month, something's wrong with your discovery or they're not actually qualified.

Should I position annuities as part of a larger retirement plan or as a standalone solution?

Always position them as one piece of a comprehensive plan. If you're only selling annuities, you're not serving the client's full needs. Show how the annuity fits alongside Social Security, portfolio withdrawals, and other income sources. This builds trust and makes you the go-to advisor for all their needs, not just the annuity guy.

How do I handle commission disclosure without making the conversation awkward?

Be direct and brief. "I'm compensated by the insurance company when you purchase this annuity. It doesn't come out of your premium-you're putting in $400,000, and $400,000 goes to work for you. My compensation is built into the pricing structure the carrier offers. I wanted you to know that upfront." Then move on. Clients respect transparency, not evasion.

Selling annuities successfully comes down to having a repeatable system that identifies the right prospects, uncovers their actual fears, and presents solutions with total transparency. The advisors writing consistent business aren't necessarily better salespeople-they're better at systematizing what works and eliminating what doesn't. If you need a proven framework to turn complex annuity concepts into clear client conversations, WebPrez gives you the video library, campaign templates, and Smart Money System to make every conversation more effective without reinventing the wheel each time.